How to Invest in Dubai Property Shares: Crowdfunding Platform Guide

Dubai real estate crowdfunding guide: how to buy Dubai property shares through SPVs, earn rental income, compare platforms, and manage risk with low minimums.

KEY takeaways

- Dubai property shares = fractional ownership via an SPV (you earn pro-rata rent + potential gains, no landlord work).

- Choose equity vs debt: equity = upside + more volatility; debt = fixed interest + borrower risk.

- Only use regulated platforms (DFSA/SCA/ADGM) and verify the license on the regulator register.

- Model net returns after all costs: fees, service charges, vacancy, management, custody, exit costs.

- Know your exit: secondary market vs hold period + vote-to-sell (liquidity varies).

- Diversify across areas/deals and start small, then scale based on real performance.

How to Invest in Dubai Property Shares: Crowdfunding Platform Guide

Buying a whole unit isn’t the only way to invest anymore. With dubai real estate crowdfunding, you can invest in Dubai property shares—small positions in real assets held by a special-purpose vehicle (SPV). You get the benefits of rent and potential capital gains without dealing with tenants, service charges, or transfer paperwork yourself.

This model fits tech-savvy investors. You onboard online, pass KYC, and view performance in a dashboard. Low minimum tickets let you start small, compare assets, and build a spread across communities, yield profiles, and hold periods. Your goal: diversify wisely and control risk, not chase headlines.

This guide provides actionable advice on leveraging these innovative crowdfunding platforms to build a diversified portfolio of Dubai property shares, generate passive income, and capitalize on Dubai's robust property growth, even with a modest initial investment. This comprehensive guide will delve into how to invest in Dubai property shares, focusing specifically on the role of crowdfunding platforms.

Why This Matters

Dubai’s market has scale and momentum. In the first half of 2025, the city recorded ~Dh431 billion of real-estate transactions, up about 25% year over year, according to DLD data reported in the press. That level of activity suggests deep demand and good liquidity for buyers and sellers.

Access barriers are falling. Traditional buying needs large down payments, bank approvals, and full ownership risk. With crowdfunding, you can start with low tickets (some platforms allow AED 500) and still participate in rental income and potential gains—without managing the asset day-to-day.

Rules protect investors. Dubai’s escrow law ring-fences off-plan buyer money. Disclosure and licensing rules at DFSA/SCA/ADGM set standards for crowdfunding operators, valuation, and investor information. Together, these frameworks help reduce information gaps and process risk.

Income still matters. Independent datasets show Dubai’s rental yields remain competitive versus many global hubs (typical residential yields often land in the mid-single-digits), which is a key reason investors look at the market for steady income.

Bottom line: You can join a large, active market with smaller amounts, clearer rails, and less admin—if you choose the right platform and deal.

Understanding Real Estate Crowdfunding

Real estate crowdfunding lets many investors pool money to buy a property together. Instead of one buyer taking a whole unit, dozens or hundreds invest small amounts and each holds a fraction. This lowers the cash barrier and spreads risk. In Dubai, the model has grown quickly because it’s digital, transparent, and open to both local and international investors with modest starting tickets.

There are two main formats: Equity and Debt. Think of them as owning vs lending.

1) Equity (Ownership)

You buy shares in an SPV (a special-purpose company) that owns the property.

- What you hold: A proportional stake in the SPV → indirect ownership of the asset.

- How you earn: Your share of net rent during the hold and profit when the asset is sold.

- Time horizon: Usually multi-year; best for those who want income and growth.

- Risk/return: Higher upside from market gains, but you share property risks (vacancy, price drops, repairs).

- Example: If you invest AED 10,000 into a AED 1,000,000 property, you own 1%. You receive 1% of rental income and 1% of sale proceeds (after costs and fees).

2) Debt (Lending)

You lend money to a developer or a property SPV and receive fixed interest.

- What you hold: A loan, not ownership.

- How you earn: Interest payments (often monthly or quarterly) for a set term.

- Time horizon: Usually shorter and defined by the loan schedule.

- Risk/return: Typically lower returns than equity, but cash flow is more predictable. You avoid direct ownership risks, though credit risk remains (can the borrower pay?).

Choosing between Equity and Debt

- Goal: Pick equity for long-term upside; pick debt for steadier, fixed income.

- Risk appetite: Equity suits higher risk, higher potential; debt suits lower volatility.

- Cash flow needs: Debt can fit investors who want regular payouts; equity works if you can wait for a larger exit later.

- Blend: Many investors mix both—use debt slices for stability and equity slices for growth.

In short, crowdfunding turns property into bite-size investments. Equity lets you grow with the market; debt pays you like a bond. Your choice depends on timeline, income needs, and risk comfort.

How Real-Estate Crowdfunding Platforms Operate in Dubai

.png)

Dubai’s real-estate crowdfunding scene blends clear rules with digital rails. Platforms sit between investors and properties, handling sourcing, vetting, legal setup, and day-to-day management so you can invest small tickets with full visibility.

Who Regulates What (the guardrails)

- DLD (Dubai Land Department): Title deeds, transfers, and escrow for off-plan projects; keeps property records clean and traceable.

- DFSA (DIFC regulator): Licenses crowdfunding operators in the DIFC; sets strict rules on disclosures, valuation, SPVs, client agreements, and conflicts.

- SCA (UAE onshore): Licenses onshore crowdfunding platforms across the UAE (outside financial free zones).

- FSRA (ADGM regulator): Covers Private Financing Platforms / private-market rails used by some SPVs.

- VARA (Dubai): Oversees virtual-asset activity; relevant when platforms use tokenisation or crypto rails.

Net effect: platforms must prove who they are, how they handle money, and how your ownership is recorded.

The Operating Model (end-to-end)

- Property sourcing

In-house teams scan developers, brokers, and data feeds to find assets that match target yields, lease terms, and risk limits.

- Due diligence

A multi-point checklist covers: legal/title, developer history, tenancy/leases, service charges, recent valuations, market comps, and technical inspections. Only properties that clear these checks go live.

- Deal setup (SPV & docs)

.png)

The platform forms a Special Purpose Vehicle (SPV)—often in DIFC or ADGM—to own the asset. It opens bank/custody accounts, lines up property management, finalises insurance, and prepares the offering pack (fees, forecasts, risks, exit).

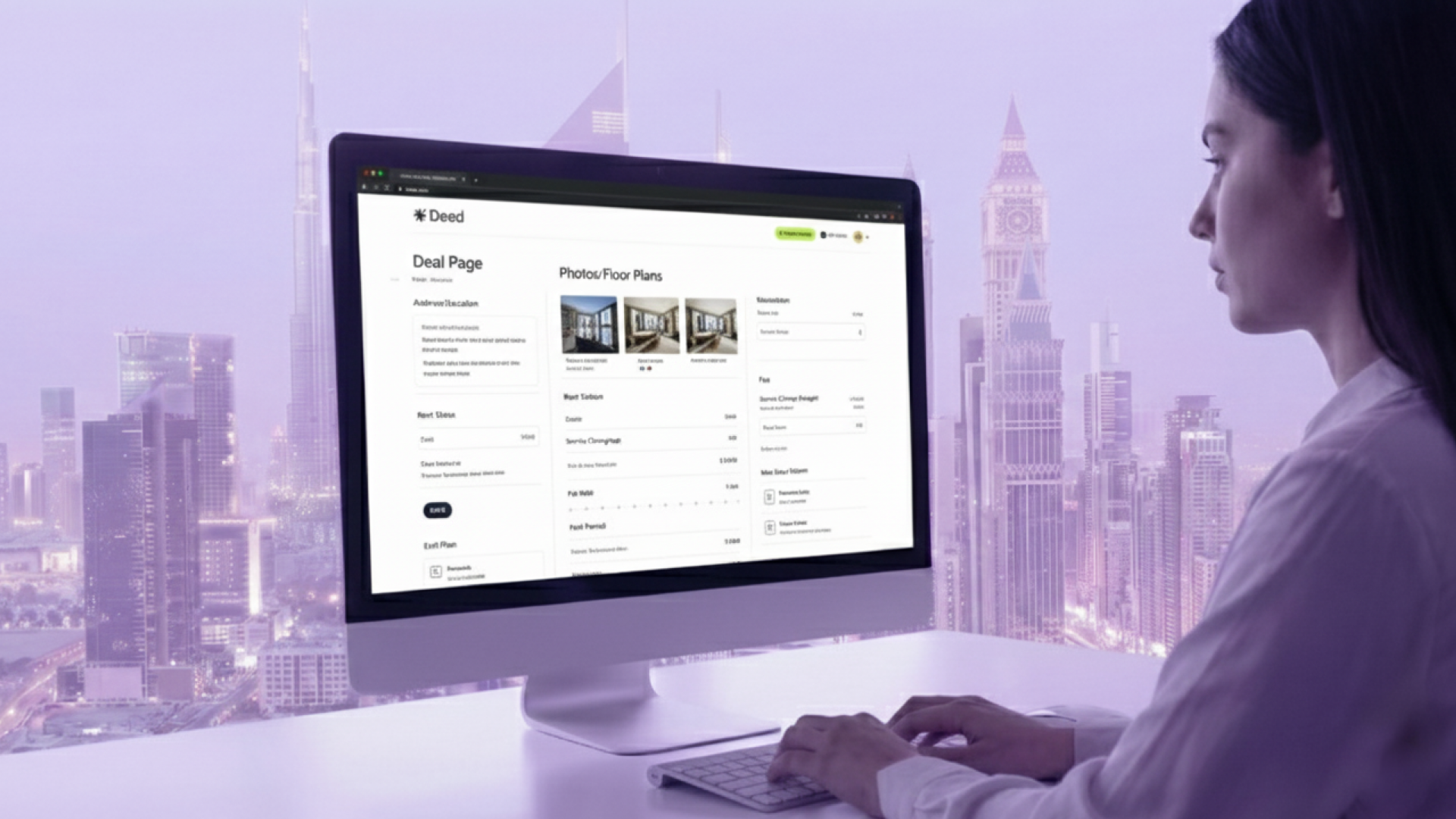

- Listing & disclosures

The deal page shows address/location, photos/floor plans, valuation date and method, rent status, service-charge budget, fee table, hold period, and exit plan. Many offer a mini data room with supporting documents.

- Investor onboarding (KYC/AML)

.png)

You sign up digitally, verify identity and source of funds, and accept platform agreements. This keeps the cap table clean and regulators happy.

- Funding & close

You subscribe online (often from AED 500–1,000 upward). Once the target is reached, funds are applied to acquire the property in the SPV’s name and the DLD transfer is completed. If the raise falls short, terms outline refunds or extensions.

- Property management & reporting

A professional manager handles tenants, rent collection, maintenance, and compliance. The platform posts monthly/quarterly dashboards: rent in/out, arrears, repairs, reserves, and any building notices.

- Income distribution

Net rental income (after service charges, management, and platform fees) is paid to investors pro-rata—typically monthly or quarterly—straight from the SPV’s ledger.

- Exit management

Exits follow one of two routes:

- Secondary market (if available): trade your shares with other investors.

- Vote to sell: the platform proposes a sale at or near the end of the hold; investors vote; proceeds are distributed pro-rata after costs.

Expect clear timelines, voting thresholds, and cost disclosures.

How Ownership Works (SPV & shares)

- You don’t usually appear on the DLD title. The SPV does.

- You own shares/units in the SPV, recorded on its cap table (and in your dashboard).

- Cash flow: Tenant → SPV account → platform ledger → your distribution, minus stated costs.

- Example: Invest 0.5% of the deal → receive 0.5% of net rent and 0.5% of sale proceeds (after fees).

Technology Stack (what makes it smooth)

- Mobile apps & dashboards: Biometric login, live balances, statements, tax/VAT invoices, and push alerts.

- Data integrations: Market comps, bank feeds, and property-management systems for up-to-date numbers.

- AI/ML assists: Screening, rent and vacancy modeling, anomaly flags on costs or arrears.

- Blockchain/tokenisation (some platforms): On-chain records for shares/tokens to improve transparency and enable peer-to-peer transfers—subject to VARA and other rules.

- E-signing & payments rails: Seamless subscriptions, dividend runs, and audit trails.

What This Means for You

- Clarity: You see the asset, the math, the fees, and the exit plan before you invest.

- Protection: Multiple regulators + DLD processes reduce paperwork risk and keep money flows controlled.

- Convenience: The platform does the heavy lifting—sourcing, diligence, tenants, and reporting—so you focus on portfolio mix and position sizes.

Bottom line: Dubai platforms combine regulated structure (SPV + disclosures) with digital convenience. You get small-ticket access to real assets, pro-rata income, and defined exits—without becoming a full-time landlord.

The 7 Checks That Matter Before You Click “Invest”

- License & regulator

Is the platform licensed by DFSA (DIFC), SCA (onshore), or operating under FSRA (ADGM)? Confirm on the regulator’s public register. If you cannot find it, pause.

- What you actually own

SPV shares vs co-title vs tokenised interest. Each has different rights and processes at exit. If tokenised, make sure it ties back to real-world records and compliant custody.

- Valuation & yield math

Who valued the property? When? Is it a desktop or full valuation? What occupancy and rent assumptions are used? DFSA rules expect robust disclosures for property crowdfunding.

- Fee stack (all-in)

.png)

Entry/arrangement fees, annual management, admin, performance (carry), bank/custody, and exit fees. Model net yield after fees—small percentages compound.

- Cash flow & custody

Which bank holds the money? How are rent, service charges, and reserves handled? How often are distributions paid?

- Exit path & liquidity

Secondary market available? Minimum hold? Vote-to-sell rules? Any penalties or spreads on resales? Tokenised rails may help, but read the fine print.

- Asset basics

Title status (completed vs off-plan), service-charge budget, tenant quality, and lease term. For off-plan exposure, confirm escrow and developer registration every time.

Platform Comparison Grid (use this to score options)

.png)

Benefits and Risks of Investing in Dubai Property Shares via Crowdfunding

Key Benefits

- Low Entry Barriers Traditional Dubai property investment requires millions of dirhams. Crowdfunding platforms allow you to start with as little as AED 500, making property investment accessible to a much broader audience.

- Professional Management Platforms handle all aspects of property management, from tenant screening to maintenance and rent collection. This provides passive income without the hassles of being a landlord.

- Diversification Opportunities With lower minimums, you can spread your investment across multiple properties, locations, and property types, reducing concentration risk significantly.

- Transparency and Data Access Digital platforms provide detailed information about each property, including financial projections, market analysis, and ongoing performance metrics.

- Regulatory Protection DFSA-regulated platforms offer institutional-grade investor protection, with segregated client funds and clear legal frameworks.

- Liquidity Options Many platforms offer secondary markets or scheduled exit windows, providing more liquidity than traditional property ownership.

Potential Risks

- Platform Risk Your investment depends on the platform's continued operation and management quality. Choose established, well-regulated platforms to minimize this risk.

- Market Risk Property values can fluctuate based on economic conditions, supply and demand, and other market factors. Dubai's property market has shown volatility in the past.

- Liquidity Risk While platforms offer more liquidity than direct property ownership, real estate remains less liquid than stocks or bonds. Exit options may be limited to specific windows or secondary market availability.

- Concentration Risk Focusing too heavily on Dubai or specific property types can expose you to localized market downturns.

- Regulatory Risk Changes in regulations could affect platform operations or investment structures, though the UAE's stable regulatory environment minimizes this concern.

Risk Mitigation Strategies

- Platform Diversification: Use multiple regulated platforms to spread platform-specific risk.

- Geographic Diversification: Invest across different areas of Dubai and other Emirates.

- Property Type Diversification: Mix residential, commercial, and alternative property types.

- Gradual Investment: Start small and increase investments as you gain experience and confidence.

- Due Diligence: Always review platform credentials, property details, and legal structures before investing.

Step-by-Step: How to Invest in Dubai Property Shares

Step 1 — Set your goal and ticket size

Income today? Balanced? Growth-tilted? Decide your first ticket (even AED-hundreds on some platforms) and your max per deal.

Step 2 — Pick 2–3 platforms

Verify license and read one full offer document on each. Bookmark the regulator pages.

Step 3 — Screen a live deal

Check valuation date, tenancy terms, service-charge budget, and the fee table. If numbers are missing, skip.

Step 4 — Complete KYC

Upload ID and proof of address; expect source-of-funds questions. This is standard.

Step 5 — Fund & subscribe

Transfer money to the platform’s instructed account (never to an individual). Save your subscription agreement, SPV share certificate, and payment proof.

Step 6 — Track distributions

Log in monthly/quarterly. Compare actual rent vs pro-forma. Read building notices (lifts, facade works, special levies).

Step 7 — Rebalance

If one asset lags, trim on the secondary market (if available) or wait for the scheduled exit. Add new slices over time to keep diversified.

Diversifying Your Property-Share Portfolio (quick playbook)

- Mix locations: Anchor in high-liquidity areas (e.g., Marina/Downtown/JVC) and add a second city when ready.

- Mix asset types: Pair long-let residential with one short-stay or logistics exposure for balance.

- Stagger holds: Blend near-term exits (2–3 years) with longer holds (4–5+ years).

- Cap concentration: Keep any single deal to ≤20% of your property-shares pot.

- Keep a cash buffer: Fees, vacancies, and special levies happen—be ready.

FAQ Section

Q1: What is the minimum investment required for Dubai property crowdfunding?

A1: The minimum investment varies by platform but can be as low as AED 500 (approximately €125 or USD 150), making it highly accessible for a wide range of investors.

Q2: Are Dubai real estate crowdfunding platforms regulated?

A2: Yes, many reputable platforms in Dubai are regulated by financial authorities like the Dubai Financial Services Authority (DFSA), providing a layer of security and transparency.

Q3: How do I earn money from crowdfunding property investments in Dubai?

A3: You can earn through two main ways: passive income from rental yields and capital appreciation when the property is sold. Some platforms also offer secondary markets for selling shares.

Q4: Is it safe to invest in Dubai property through crowdfunding?

A4: While all investments carry risk, regulated platforms conduct thorough due diligence and manage properties professionally, mitigating some risks. It's crucial to choose regulated platforms.

Q5: Can foreigners invest in Dubai property crowdfunding?

A5: Yes, most platforms allow both residents and non-residents, including foreigners, to invest. You typically need to be over 18 and have a valid passport.

Q6: What are the potential returns on Dubai property crowdfunding investments?

A6: Returns typically come from two sources: (1) your share of net rental income paid out by the SPV/platform, and (2) capital gains (or losses) when the property is sold. In Dubai, many residential deals are underwritten around mid-single-digit rental yields, but your actual return depends on fees, vacancy, service charges, and the exit price

Q7: What happens if the property loses value?

A7: In an equity model, if the property loses value, your investment may also decrease. This is a market risk inherent in real estate. Debt models typically offer more protection against property value fluctuations.

DEED's Take

At Deed, we've experienced firsthand the frustrations of traditional real estate investment. As tech professionals and investors ourselves, we were tired of the outdated processes, high barriers, and lack of transparency that characterized property investment.

We built Deed to solve these fundamental problems and create the platform we always wanted to use. Our mission is simple: make property investment as accessible, transparent, and efficient as investing in stocks.

Our Technology-First Approach

Mobile-Native Design: Every feature is designed for mobile-first use, from account creation to portfolio management. We believe your phone should be your primary investment tool.

Regulatory Excellence: We chose DFSA regulation and DIFC structuring because we understand that trust and legal protection are non-negotiable for serious investors.

Transparency by Default: We provide comprehensive data on every property, clear fee structures, and real-time performance tracking because informed investors make better decisions.

Accessibility Without Compromise: Our AED 500 minimum doesn't mean lower quality. We maintain the same rigorous standards for all investments, regardless of size.

How Deed Empowers Your Investment Journey

With Deed, you can build a sophisticated property portfolio with the same ease and precision you use to manage your stock investments. Our platform provides the tools, data, and access you need to make informed decisions and achieve your investment goals.

Conclusion

Investing in Dubai property shares through crowdfunding platforms offers an unparalleled opportunity to access one of the world's most vibrant real estate markets with unprecedented ease and affordability. This guide has illuminated the mechanisms of fractional ownership, highlighted leading platforms, and outlined the critical benefits and risks involved. By leveraging these innovative platforms, investors can build diversified portfolios, generate passive income, and capitalize on Dubai's robust property appreciation, all while mitigating the traditional complexities of real estate ownership.

The Dubai real estate market continues to demonstrate resilience and growth, driven by strong economic fundamentals and a forward-thinking regulatory environment. For those looking to expand their investment horizons, crowdfunding presents a compelling pathway to participate in this dynamic sector. Don't miss out on the opportunity to grow your wealth in a market that consistently delivers impressive returns. Explore reputable Dubai property crowdfunding platforms today and take the first step towards securing your financial future in this thriving global hub.

__________________________________________________

For promotional purposes only. Property and other details may vary. Capital at risk. Deed is regulated by the DFSA.

Senior Growth, Marketing & Brand Manager | Elevating Brand Equity & Fueling Sales Growth Across Fintech, Proptech.

Signup to our newsletter!

Stay ahead with exclusive updates, insights, and opportunities delivered straight to your inbox.

Frequently Asked Questions

Start earning passive income today

Join thousands of investors building wealth through fully-managed rental properties.