How to Invest in Dubai Real Estate as a Foreign Investor: Legal Requirements and Process

Learn how foreign investors can legally buy property in Dubai, including freehold zones, visa options, full buying process, and true costs to budget for.

KEY takeaways

How to Invest in Dubai Real Estate as a Foreign Investor: Legal Requirements and Process

Summary

Dubai’s appeal is clear: a stable legal system, strong infrastructure, and liquid property market that welcomes international buyers. The good news for you as a foreign investor is simple: you can own. The fine print matters though—what you can buy, how you pay, which visa to choose, and what it all costs.

This guide outlines the essential legal requirements, streamlined processes, and key considerations, including ownership types, associated costs, and market insights, to help you navigate the vibrant Dubai property market with confidence and achieve your investment goals.

Why This Matters

Dubai’s property market isn’t just for the ultra-wealthy. Clear rules, designated freehold zones, and investor-friendly visas make ownership realistic for international buyers. For many, one purchase delivers two wins: steady rental income and a path to UAE residency.

Recent figures point to real scale and staying power: the UAE real estate market is projected to reach about US$693.5B in 2025, with housing around US$401.8B, and an expected 2.28% annual growth through 2029. Add the Golden Visa for qualifying property owners (with long-term residency benefits) and shorter investor options at lower thresholds, and the case gets even stronger.

This guide walks you from interest to keys in hand—what you can own as a foreign buyer, the fees to budget for, and the visa steps to consider—so you can invest in Dubai with clarity and confidence.

Can a Foreigner Really Buy Property in Dubai?

Yes, absolutely. Foreign nationals, even those who do not reside in the UAE, can purchase property with full ownership rights in specific areas designated as freehold zones. This was a landmark decision that opened Dubai's market to the world and remains the cornerstone of its success.

It's important to understand the two main types of property ownership available to foreigners:

Freehold: This is the most common and desirable form of ownership. When you buy a freehold property, you own the building and the land it stands on outright. You have the right to sell, lease, or inherit the property without any restrictions. There are over 60 designated freehold areas in Dubai, including popular communities like Dubai Marina, Downtown Dubai, and Palm Jumeirah.

Leasehold: With leasehold ownership, you own the right to use the property for a fixed term, typically up to 99 years. You do not own the land itself. While less common for residential purchases, it's an option in certain areas.

Foreign nationals can buy property in Dubai in designated freehold areas, and ownership can be freehold (full ownership) or leasehold/usufruct (long-term use rights), depending on the property. [Source: Dubai Gov]

Popular Freehold Areas for Foreign Investors

Understanding where you can buy is crucial for making the right investment decision. Dubai has designated over 60 freehold areas where foreign nationals can purchase property with full ownership rights. Here are some of the most popular and investment-worthy locations:

Downtown Dubai

It is the heart of the city, home to the Burj Khalifa and Dubai Mall. Properties here offer excellent rental yields and strong capital appreciation potential. The area attracts both tourists and business professionals, making it ideal for short-term and long-term rentals.

Dubai Marina

This is a waterfront community known for its high-rise apartments and vibrant lifestyle. It's particularly popular with young professionals and offers some of the best rental yields in the city. The area has excellent connectivity to business districts and entertainment venues.

Palm Jumeirah

It represents the pinnacle of luxury living in Dubai. This man-made island offers exclusive villas and apartments with private beach access. While property prices are higher, the area commands premium rental rates and has shown strong appreciation over time.

Jumeirah Village Circle (JVC)

This is an emerging area that offers more affordable entry points for investors. It's popular with families and young professionals, offering good rental yields and potential for capital growth as the area develops.

Business Bay

It is Dubai's central business district, making it highly attractive for rental investments. The area offers a mix of residential and commercial properties, with excellent connectivity to other parts of the city. [Source: Driven Properties, 2025]

The Step-by-Step Process for Foreign Buyers

Buying property in Dubai follows a clear, regulated path. The goal is simple: protect both buyer and seller and make the transfer traceable. Working with a RERA-registered agent and a legal advisor is strongly recommended.

Step 1: Set your budget and goals

Decide why you’re buying: rental income, capital growth, holiday home, or future move-in.

Calculate your total budget, not just the price. Add typical purchase costs of ~7–8% (DLD transfer fee, trustee fee, title deed admin, and agent commission).

If you plan to finance, get a bank pre-approval so you know your exact limit and timeline.

Quick checklist

- Target price range and building/year

- Cash vs bank finance (pre-approval letter if financing)

- Estimated fees and reserves for furniture, snagging, and first-year service charges

Step 2: Find the right property (and confirm what you can buy)

Ask your agent to show options in designated freehold areas and share recent deals in the same building or street. Shortlist a few units and compare service charges, condition, view, and rental demand.

You’ll see three ownership/use models:

- Freehold: Full ownership of the unit (and the land share).

- Usufruct/Leasehold: Long-term use rights (often up to 99 years).

- Off-plan: Buying under construction from a developer. Payments must go into a RERA-regulated escrow account (required by law).

Tip (off-plan): Before paying anything, confirm the project is registered and the escrow account is active with DLD/RERA. Ask for the escrow details in writing and verify them.

Step 3: Negotiate and sign the Memorandum of Understanding (MoU / RERA Form F)

Once you choose a unit, your agent drafts RERA Form F (MoU). This document sets price, dates, inclusions, and who pays which fees. Read it line by line.

- You’ll place a security deposit (often 10%).

- It’s held securely (commonly by the trustee office or broker per process) until transfer.

- If you’re financing, add a clause for bank valuation and final loan approval.

What to confirm in the MoU

- Final price and payment method (cash or mortgage)

- What furniture/appliances stay

- Deadlines for NOC, valuation, and transfer

- Penalties for delay by either side

Step 4: Clearances and the Developer NOC

Before transfer, the seller must secure a No-Objection Certificate (NOC) from the developer.

This proves service charges are paid and the developer has no claim on the unit.

There’s a NOC fee (varies by developer). Your agent will schedule the NOC appointment and guide documents needed.

If you’re financing:

- Your bank arranges valuation and issues a final offer letter.

- Coordinate with the trustee office so funds, cheques, or bank manager’s cheques are ready on the day of transfer.

Step 5: Transfer and Title Deed at the Dubai Land Department (via a Trustee Office)

Both parties (or their authorized representatives via Power of Attorney) meet at a DLD-approved trustee office to complete transfer.

Bring:

- Original passports (buyer and seller)

- Signed MoU (Form F)

- Developer NOC

- Proof of purchase funds / cheques (and mortgage documents if applicable)

Pay on the day:

- DLD transfer fee: 4% of the purchase price

- Trustee office fee (fixed schedule; varies by property value)

- Title deed admin fee

- Agent commission (if not already settled)

- Mortgage registration fee if you’re financing (typically 0.25% of the loan amount + admin)

Once processed, DLD issues the Title Deed (electronically and/or paper depending on service). This is your proof of ownership.

After Transfer: What to do next

- Utilities: Set up DEWA (electricity/water) and any cooling provider.

- Service charges: Register your ownership with the building/community and keep service charges current.

- If you plan to rent: Register the tenancy on Ejari and keep copies of contracts and receipts.

- Records: Keep a secure folder with MoU, NOC, payment proofs, title deed, service charge statements, and any warranties/snags.

Mini due-diligence list (ready property)

- Latest service-charge statement

- Maintenance history and any ongoing building works

- Rental history (if tenanted) and notice terms

- Outstanding liens or developer balances

Mini due-diligence list (off-plan)

- Developer registration and project escrow details

- Payment plan vs construction milestones

- Oqood/off-plan registration status

- Handover timeline and snagging policy

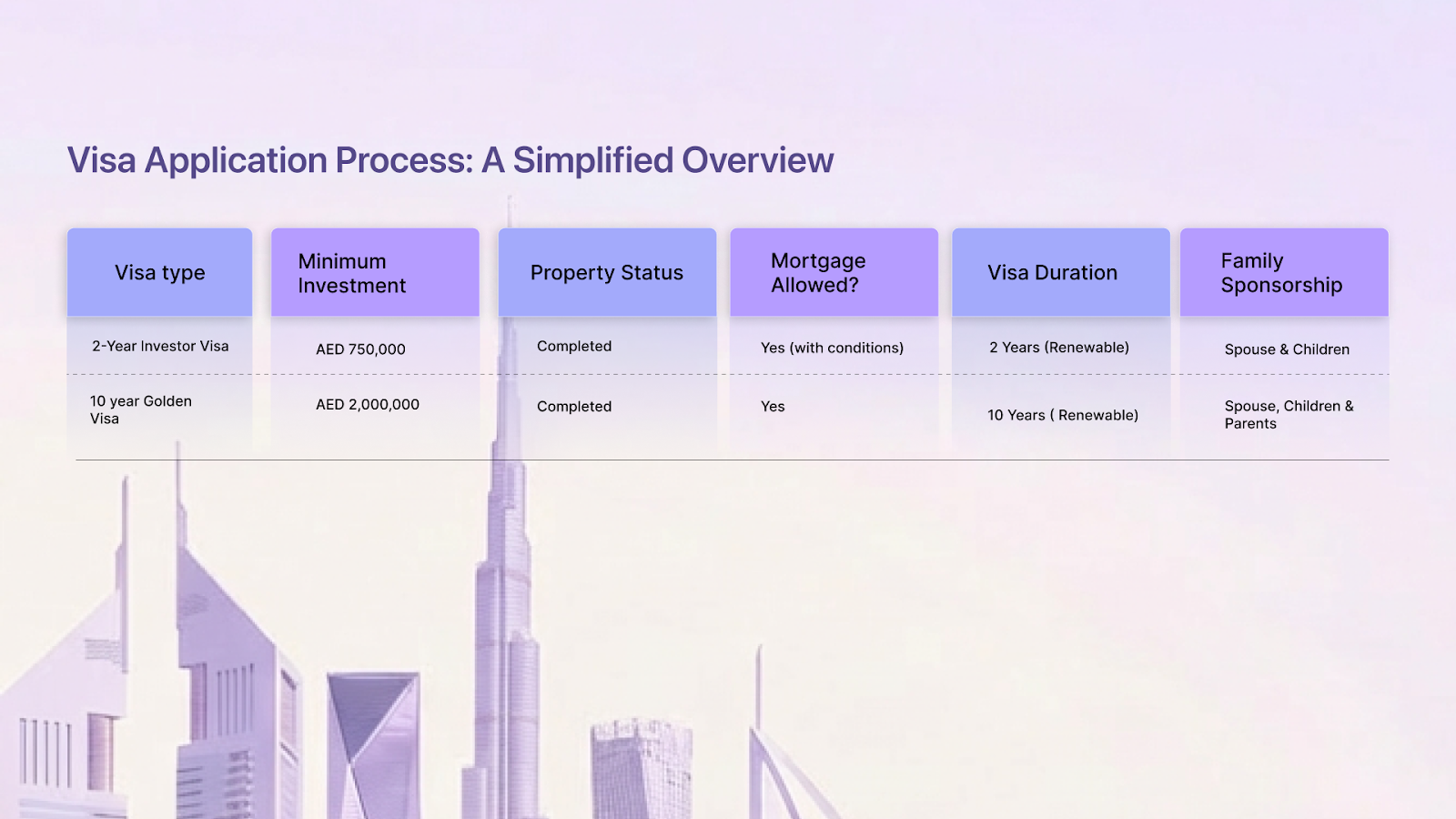

Understanding Dubai Real Estate Investment Visas

One of the most attractive aspects of investing in Dubai real estate is the opportunity to obtain a residency visa based on your property investment. The UAE offers two main visa options for property investors, each with different requirements and benefits.

1. The 2-Year Property Investor Visa

This is a popular option for investors making a mid-level investment. It provides a renewable, two-year residency visa for the property owner.

Key Requirements:

- Minimum Investment: You must own a property with a minimum value of AED 750,000 (approximately $204,000 USD).

- Ownership: The property must be fully owned and not be off-plan. If the property is mortgaged, at least 50% of the value (or AED 750,000) must be paid off. A letter from the bank will be required.

- Joint Ownership: A husband and wife can share in one property to meet the minimum investment threshold. [Source: Dubai Land Department]

2. The 10-Year Golden Visa

The Golden Visa is a long-term residency visa that offers greater stability and benefits. It is designed for those making a more substantial investment in the Dubai property market.

Key Requirements:

- Minimum Investment: You must own a property (or a portfolio of properties) with a minimum value of AED 2 million (approximately $545,000 USD).

- Ownership: The property can be off-plan or completed, and it can be mortgaged. The investment must be held for at least three years.

- Benefits: The Golden Visa covers the investor, their spouse, children, and parents, offering a comprehensive residency solution for the entire family. [Source: UAE Government Official Portal]

Visa Application Process: A Simplified Overview

The application process for both visas is managed through the Dubai Land Department (DLD) and the General Directorate of Residency and Foreigners Affairs (GDRFA).

- Submit Application: Apply through the DLD's service centers or the Dubai REST app.

- Provide Documents: You will need your passport, the property Title Deed, a personal photo, and valid health insurance.

- Medical Fitness Test: All applicants for residency visas must undergo a medical fitness test at a government-approved health center.

- Visa Stamping: Once approved, your visa will be stamped into your passport.

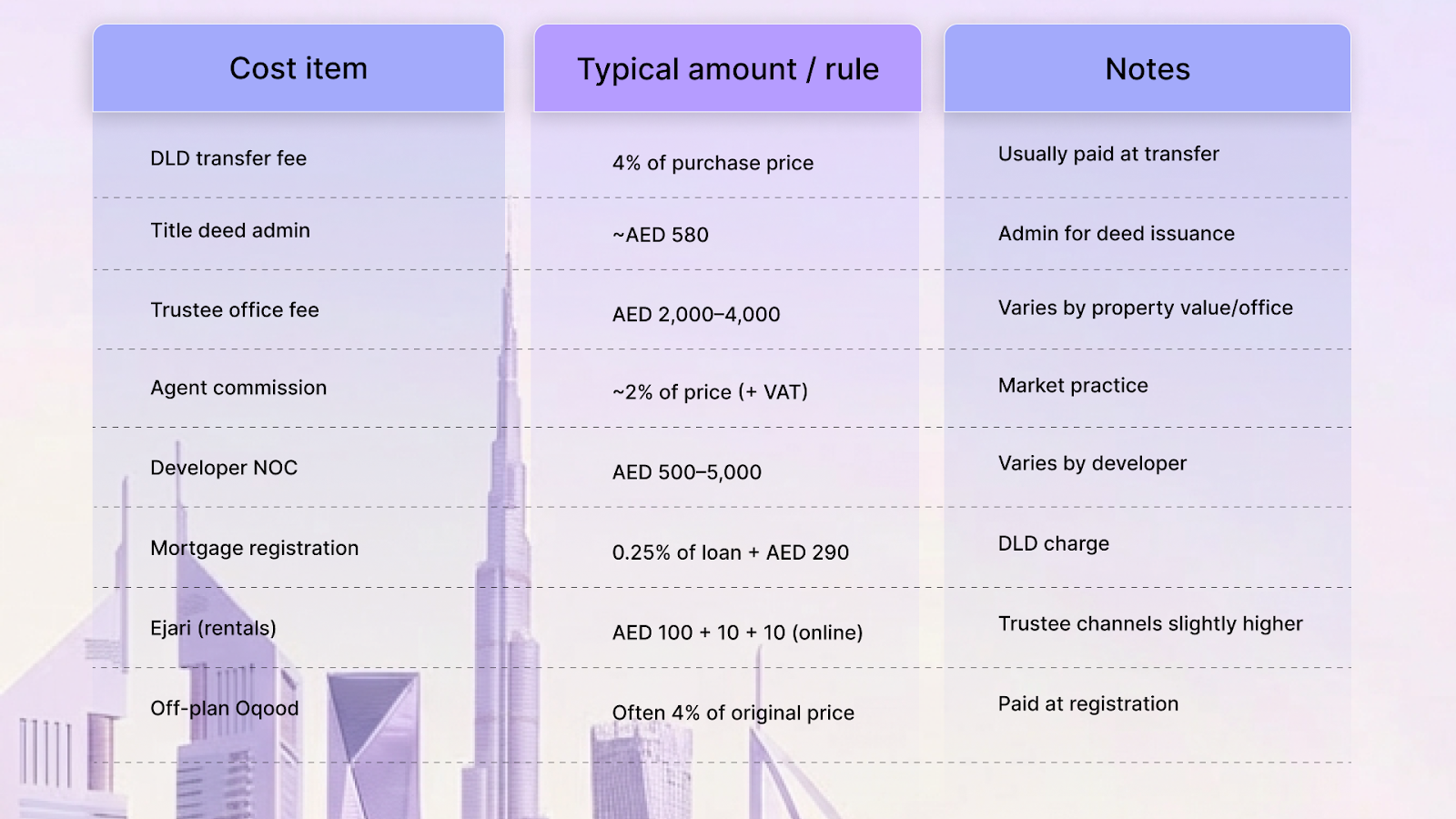

Understanding the Costs Involved

When budgeting for your Dubai property investment, it's essential to understand all the costs involved beyond the purchase price. Here's a breakdown of the main expenses:

Purchase Costs

- Dubai Land Department Transfer Fee: 4% of the property purchase price

- Real Estate Agent Commission: Typically 2% of the purchase price

- Mortgage Registration Fee: 0.25% of the loan amount (if applicable)

- Valuation Fee: AED 2,000-5,000 for property valuation

- Legal Fees: AED 5,000-15,000 for legal representation

Ongoing Costs

- Service Charges: Annual fees for building maintenance and amenities (varies by property)

- DEWA Connection: Electricity and water connection deposit (AED 2,000 for apartments, AED 4,000 for villas)

- Property Management: 5-10% of annual rental income if using a management company

- Insurance: Property insurance is recommended but not mandatory

To summarise- Costs & Fees (typical ranges):

Numbers above are indicative. Always check the latest fees at DLD/Trustee before transfer.

Financing Options for Foreign Buyers

Many international banks and UAE-based banks offer mortgage financing to foreign property buyers. Here are the key points to understand:

Mortgage Eligibility

- Down Payment: Foreign buyers typically need to provide 25-30% down payment for completed properties

- Income Requirements: Banks usually require a minimum monthly income of AED 15,000-20,000

- Documentation: You'll need salary certificates, bank statements, and proof of employment

- Interest Rates: Current rates range from 3.5% to 6% depending on the bank and your profile

Popular Banks for Foreign Buyers

Several banks in the UAE specialize in providing mortgages to non-resident foreign buyers:

- Emirates NBD: Offers competitive rates and has experience with international clients

- ADCB: Provides mortgages for both residents and non-residents

- HSBC UAE: Leverages its global presence to serve international buyers

- Mashreq Bank: Offers flexible terms for foreign investors

Dubai Real Estate Market: Statistics and Trends

Dubai’s property market is active, liquid, and well regulated. The numbers point to steady growth and a wide range of entry points for buyers.

At a glance

- H1 2025 activity: Total real estate transactions exceeded AED 431B; the investment market attracted 94,717 investors who completed 118,132 investments worth ~AED 326B. (Source: Dubai Government)

- Q1 2025 residential sales: ~42,200 residential sales transactions with AED 114.4B total sales value. (Source: Cavendish Maxwell report)

- Supply pipeline: ~73,200 residential units are projected for delivery in 2025 (report projection). (Source: Cavendish Maxwell report)

- Rental yields (citywide, gross): 7.3% for apartments and 5.0% for villas/townhouses (as of end of Q1 2025). (Source: Cavendish Maxwell report)

What’s driving the market

- Global hub: Strategic location and strong connectivity keep demand broad and year-round.

- Policy and transparency: Clear rules, regulated escrow for off-plan, and documented transfer steps build trust.

- Infrastructure and lifestyle: Master-planned communities, amenities, and tourism support both use and yield cases.

- Financing access: Competitive banking and established mortgage processes support qualified buyers.

- Income potential: Dubai’s gross rental yields are typically mid-to-high single digits (varies by area and unit type).

- Capital growth (off-plan): Off-plan pricing can move between launch and handover, but the uplift is not a fixed %.

Bottom line

Dubai offers a diverse price ladder and clear rules, with demand led by both end-users and international investors. If you match area, asset quality, and holding period to your goal, the market provides credible options for income and long-term value.

FAQ Section

Q1: Do I need to be a resident of Dubai to buy property?

A1: No, foreign investors do not need to be residents of Dubai to purchase property. The UAE government has implemented policies that allow non-residents to own freehold properties in designated areas. Furthermore, property ownership can even lead to eligibility for long-term residency visas, such as the 10-year Golden Visa for investments over AED 2 million.

Q2: What are the main taxes associated with buying property in Dubai?

A2: Dubai offers a highly attractive tax environment for real estate investors. There is no annual property tax on residential properties, no capital gains tax on property sales, and no income tax on rental earnings. The primary cost is a one-time Dubai Land Department (DLD) registration fee of 4% of the property's value, paid upon transfer of ownership.

Q3: What is the difference between freehold and leasehold property in Dubai?

A3: Freehold ownership grants complete and perpetual ownership of both the property and the land it occupies, offering full control. Leasehold ownership, conversely, grants rights to the property for a specific period, typically up to 99 years, with the land remaining under developer or government ownership. Freehold is generally preferred for long-term investment.

Q4: How can I ensure a smooth property purchase process as a foreign investor?

A4: To ensure a smooth process, it is highly recommended to engage a RERA-certified real estate agent. They will guide you through property selection, legal requirements, paperwork, and negotiations. Additionally, understanding the DLD regulations, securing necessary financing, and conducting thorough due diligence on the property and developer are crucial steps.

Q5: What are the potential returns on investment in Dubai real estate?

A5: Dubai real estate offers competitive returns. Rental yields typically range from 5% to 8% annually. For off-plan properties, capital appreciation can be significant, often reaching 5% to 10% annually, with some properties seeing 15% to 30% growth from construction start to handover. The market's stability and growth drivers contribute to attractive long-term prospects.

Q6: Are there any restrictions on reselling property in Dubai?

A6: Reselling property in Dubai is generally straightforward and less complicated than in many other countries. There are no specific restrictions on reselling. The process typically involves a reservation agreement, obtaining a No Objection Certificate (NOC) from the developer, and completing the transfer at the Dubai Land Department Trustee office with the assistance of real estate agents.

Q7: Can I get a mortgage in Dubai as a foreign investor?

A7: Yes, foreign investors can obtain mortgages in Dubai. Local and international banks offer financing options, though the terms might differ from those in your home country. Mortgage terms are typically shorter, ranging from 10 to 25 years. It's advisable to consult with a financial advisor or mortgage broker specializing in Dubai real estate to explore suitable options.

How Deed Can Help

If you want exposure to Dubai real estate without buying an entire unit, Deed lets you invest via fractional shares in income-generating residential properties — starting from AED 500.

What you get with Deed:

- Lower entry point: Start small and build gradually instead of waiting to fund a full purchase.

- Monthly rental income (pro-rata): Earn rental payouts in proportion to your shares, while the property is managed end-to-end.

- Fully digital experience: Invest in minutes and track performance in the app/dashboard.

- Regulated platform: Deed states it is DIFC-based and DFSA-regulated.

Important note (to keep it compliant): fractional investments are designed for investment access and diversification — they are not presented as a route to UAE property investor visas (visa eligibility depends on property ownership and DLD/GDRFA rules).

Conclusion

Investing in Dubai's real estate market presents a compelling opportunity for foreign investors seeking high returns, a stable economic environment, and significant tax advantages. The process is streamlined and transparent, with clear legal frameworks and a supportive government ecosystem. By understanding the key steps, from engaging a RERA-certified agent to navigating the DLD registration process, investors can confidently enter this dynamic market. The availability of long-term residency visas further enhances the appeal, offering a gateway to a vibrant and cosmopolitan lifestyle.

Ready to explore the lucrative world of Dubai real estate? Take the first step towards building your international property portfolio in one of the world's most exciting markets.

__________________________________________________

For promotional purposes only. Property and other details may vary. Capital at risk. Deed is regulated by the DFSA.

Senior Growth, Marketing & Brand Manager | Elevating Brand Equity & Fueling Sales Growth Across Fintech, Proptech.

Signup to our newsletter!

Stay ahead with exclusive updates, insights, and opportunities delivered straight to your inbox.

Frequently Asked Questions

Start earning passive income today

Join thousands of investors building wealth through fully-managed rental properties.