How to Calculate and Track Monthly Income from Dubai Property Investments

Learn how to calculate and track monthly income from Dubai property with net yield formulas, expense checklists, vacancy buffers, and ROI tools.

KEY takeaways

How to Calculate and Track Monthly Income from Dubai Property Investments

Income investing is simple in theory: buy a property, collect rent. In practice, your monthly income from Dubai property rises or falls on small details—service charges, periods without tenants, short-term cleaning costs, or a rent cheque that arrives late. One missed line can turn a great yield into an average one.

This guide provides a comprehensive overview of how to calculate and effectively track monthly income from Dubai property investments. It details essential financial metrics, outlines common expenses, and offers actionable strategies to maximize rental yields, ensuring investors can make informed decisions and achieve consistent returns in Dubai's dynamic real estate market.

Why This Matters

For any serious real estate investor, tracking monthly income is not just about seeing money come in—it is about understanding the true performance of your assets. In a market as dynamic as Dubai, where rental yields average 6-7% and can climb higher in prime locations, precise income tracking is the foundation of smart investment management. It allows you to move beyond simple revenue collection and gain a clear, real-time picture of your investment's financial health.

Without accurate tracking, you are essentially flying blind. You might overlook hidden costs that erode your profits, miss opportunities to optimize rental rates, or fail to identify underperforming assets. By implementing a systematic approach to income and expense tracking, you can make data-driven decisions that protect your capital, enhance your returns, and ensure long-term profitability. This guide will show you how to do just that.

Understanding the Components of Monthly Income: A Detailed Breakdown

To track monthly income from a Dubai property accurately, look beyond the headline rent. Map every inflow and outflow tied to the unit. That full picture is the base for smart decisions and realistic forecasts.

Primary income vs. add-ons

Your revenue usually has one core stream plus several helpful extras.

1) Base monthly rent

- Defined in the Ejari-registered lease.

- Most predictable line item.

- Typical annual ranges (indicative):

- Studios: AED 35,000–50,000

- 1-bed: AED 50,000–80,000

Convert to monthly by dividing by 12 when you track cash flow.

2) Advance rent payments (post-dated cheques)

- Tenants often pay quarterly, bi-annually, or even annually.

- For accounting, recognize it monthly.

- Example: You receive AED 90,000 upfront for a year → record AED 7,500/month.

3) Security deposit (liability, not income)

- Held to cover damages; normally refundable at lease end.

- Best practice: keep in a separate account so it isn’t counted as revenue.

4) Parking & storage

- Can boost cash flow, especially in premium areas.

- Parking: AED 1,000–3,000/month

- Storage: AED 200–500/month

5) Utility reimbursements

- If your lease says the tenant reimburses DEWA/district cooling, record these as income to offset the matching expense.

- If you pay utilities during vacancy, record as your expense (see below).

6) Late/administrative fees

- Late payment penalties, bounced cheque charges, renewal admin fees.

- Not ideal to “plan” on, but do record them when they occur.

Expense categories that move your net income

Expenses determine what’s left after rent. Track both fixed and variable costs.

A) Fixed monthly (predictable)

Service charges

- For building/community upkeep (security, common areas, amenities).

- Often billed annually at AED 8–15/sq ft/year.

- Accrue monthly for clean books (annual ÷ 12).

Property management fee

- Typically 5%–10% of collected rent.

- Example: Monthly rent AED 7,500 → fee AED 375–750.

Insurance

- Comprehensive policy AED 1,500–3,000/year.

- Record monthly (annual ÷ 12).

Mortgage payment (if financed)

- Split into principal and interest for proper tracking.

- Principal builds equity; interest is an expense.

B) Variable / intermittent (plan ahead)

Maintenance & repairs

- Budget 1%–2% of annual rent into a monthly reserve.

- Covers minor fixes and occasional replacements.

Utilities (owner-paid periods)

- During vacancy, you’ll cover utilities/service fees.

- Record as expenses when they hit.

Marketing & leasing

- Listing fees, pro photos, vacancy promos.

Legal & professional

- Lease disputes, contract reviews, accounting support.

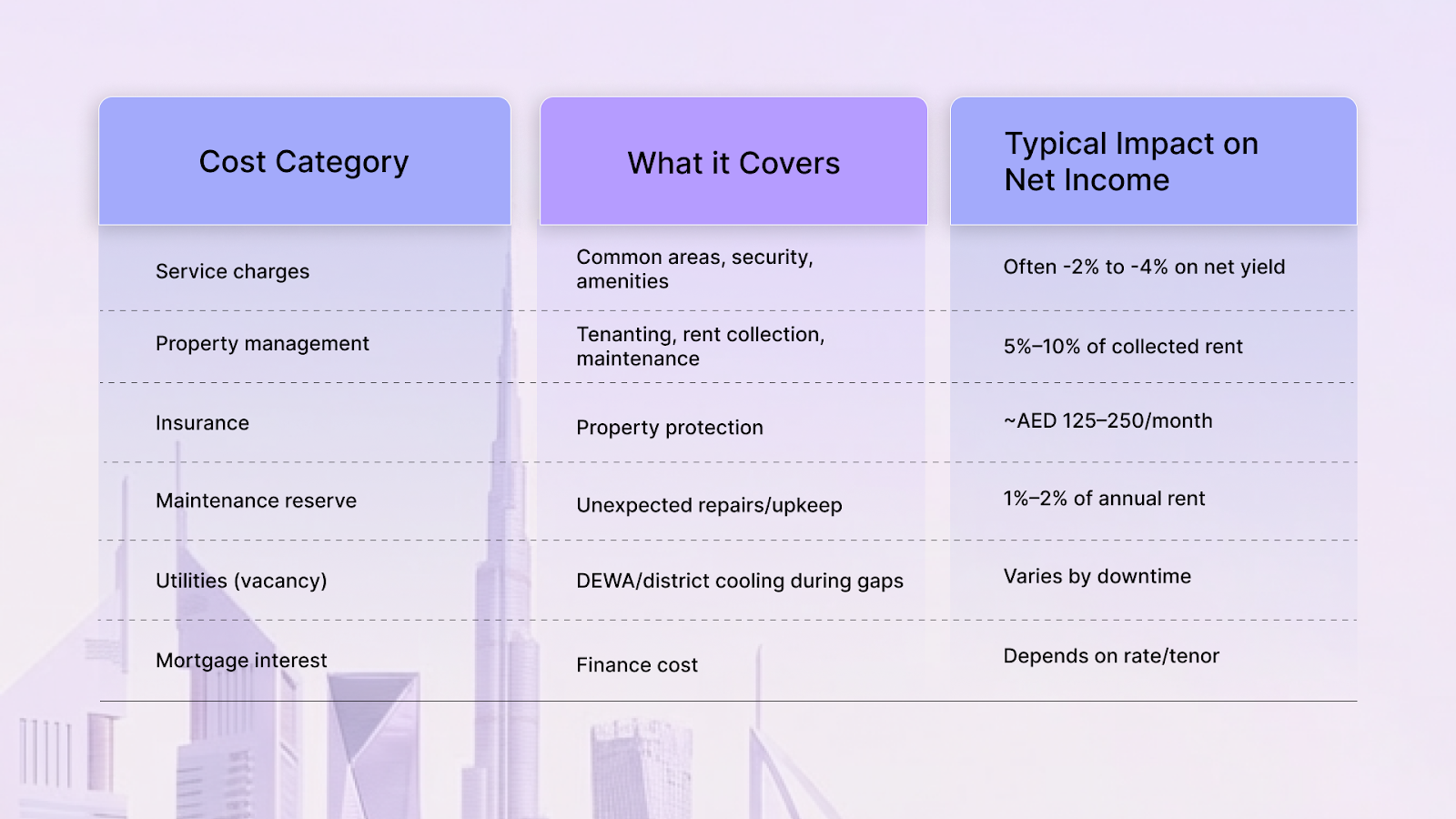

Quick reference: costs that eat into net returns

- What it covers: Annual building & community upkeep (security, cleaning, landscaping, common areas).

- Typical impact on net income: AED 10 – 30 per sq ft per year depending on community & amenities. (Driven Properties: Service Charge Index (DrivenProperties))

- What it covers: Tenant sourcing, rent collection, upkeep coordination.

- Typical impact on net income: 5 – 10% of annual rent for long-term leases. (Engel & Völkers: Management Fee Structure (Engel & Völkers))

- What it covers: Repairs/upkeep not covered by tenant; routine wear & tear.

- Typical impact on net income: 1 – 3% of rental income budgeted annually. (JX Estates: Financial Management (JX Estates))

- What it covers: Building & liability protection (fire/theft/liability).

- Typical impact on net income: Varies by coverage/size — part of ongoing expense planning (industry standard). (Rental Yield Guides (Wise))

- What it covers: DEWA & district cooling while unoccupied.

- Typical impact on net income: Varies by downtime & usage — variable cost during vacancy periods. (Standard utility cost principle)

- What it covers: Finance cost of interest on a mortgage.

- Typical impact on net income: Depends on loan rate & tenor — major influence if leveraged. (Finance cost principle)

- What it covers: Dubai Municipality 5% housing levy (paid via DEWA bill).

- Typical impact on net income: 5% of annual rent (charged monthly). (Springfield Properties: Property Tax Explained (SpringField Properties))

Tip: Build a “vacancy buffer” of 1–2 months of rent per year into your pro-forma. If the unit stays occupied, that buffer becomes upside.

Essential Calculation Methods for Monthly Income

The math isn’t complex, but consistency is everything. Use the same formulas each month to spot trends and fix issues early.

1) Net monthly income (cash flow)

Formula

Net Monthly Income = Gross Monthly Income – Total Monthly Expenses

Worked example (Dubai Marina 1-bed):

Gross income

- Base rent: AED 8,500

- Parking: AED 1,000

- Storage: AED 300

- Total gross = AED 9,800

Expenses

- Service charges: AED 15,000/year ÷ 12 = AED 1,250

- Property management: 7% × 8,500 = AED 595

- Insurance: AED 2,400/year ÷ 12 = AED 200

- Maintenance reserve: AED 400

- DEWA admin/connection: AED 50

- Total expenses = AED 2,495

Net monthly income

- AED 9,800 – AED 2,495 = AED 7,305

That’s your true monthly profit after core costs.

2) Rental yield (compare deals apples-to-apples)

Gross rental yield

Gross Yield = (Annual Rent ÷ Purchase Price) × 100

Example:

- Price AED 1,200,000

- Annual rent AED 102,000 (8,500 × 12)

- Gross yield = (102,000 ÷ 1,200,000) × 100 = 8.5%

Net rental yield

Net Yield = ((Annual Rent – Annual Expenses) ÷ Purchase Price) × 100

Example:

- Annual rent AED 102,000

- Annual expenses AED 24,000

- Net income AED 78,000

- Net yield = (78,000 ÷ 1,200,000) × 100 = 6.5%

Rule of thumb: In Dubai, net ≈ gross – 1.5% to 2% (varies by service charges and management).

3) ROI (include rent and price growth)

ROI (multi-year)

ROI = ((Total Return – Total Investment) ÷ Total Investment) × 100

5-year example:

- Purchase price: AED 1,200,000

- Rental income (5 years): AED 390,000

- Sale price: AED 1,500,000

- Capital gain: AED 300,000

- Total return = 390,000 + 300,000 = AED 690,000

- ROI = (690,000 ÷ 1,200,000) × 100 = 57.5% over 5 years

- ≈ 11.5% average per year

Add stamp/transfer fees, fit-out, and financing costs to your total investment for a truer ROI.

4) Handling advance cheques correctly

If you receive AED 90,000 upfront for the year:

- Cash flow (month 1): +90,000

- Recognized income each month: 7,500

- Don’t inflate a single month’s P&L just because cash arrived. This keeps your monthly performance accurate and your year-to-date on track.

5) Vacancy & break-even math

Break-even monthly rent

Break-even = Fixed Monthly Costs + Average Monthly Variable Costs

If your fixed + variable average = AED 6,800, any rent above that is profit.

Plan for 1–2 months vacancy: divide your annual net income by 10 or 11 months to stress test yield.

6) Debt metrics (for financed buyers)

- Interest coverage ratio (ICR)

ICR = Net Operating Income ÷ Interest Expense

Aim for >1.5–2.0× for comfort with rising rates.

- Loan-to-value (LTV)

Lower LTV = lower risk and stronger cash flow. UAE expat mortgages usually start at 20% down.

7) Monthly tracking checklist (10-minute routine)

- Update rent received (per lease schedule).

- Record ancillary income (parking, storage, reimbursements).

- Log all expenses paid (management, insurance, maintenance).

- Recalculate net income and running YTD.

- Re-forecast next month for vacancy or renewals.

- Flag overdue items (late fees, bounced cheques).

Tip: Use a simple spreadsheet or app (property management software or even a budget app). The key is consistency.

Example: monthly tracker template (copy/paste)

Income

- Base rent: ______

- Parking: ______

- Storage: ______

- Utilities reimbursed: ______

- Other fees: ______

- Gross income: ______

Expenses

- Service charges (annual ÷ 12): ______

- Management fee: ______

- Insurance (annual ÷ 12): ______

- Maintenance reserve: ______

- Mortgage: Principal _____ | Interest _____

- Utilities (owner-paid): ______

- Marketing/Leasing: ______

- Legal/Professional: ______

- Total expenses: ______

Net monthly income = Gross – Expenses: ______

Running YTD net: ______

Vacancy buffer balance: ______

Common pitfalls (and quick fixes)

- Counting deposits as income → Keep deposits in a separate account.

- Ignoring service charges → Annual ÷ 12 into monthly P&L.

- Under-budgeting maintenance → Set aside 1%–2% of annual rent monthly.

- No vacancy planning → Hold 1–2 months rent in reserve.

- Not separating principal vs. interest → You’ll misread cash flow health.

What “good” looks like (benchmarks to aim for)

- Collection rate: ≥ 98% on-time rent.

- Occupancy: 90%–95%+ annually (market & area dependent).

- Net yield: 5.5%–7.5% on standard apartments (varies by area/fees).

- ICR: >1.5× if financed.

- Maintenance: within your 1%–2% reserve.

Bottom line

Your monthly income is more than rent—it’s rent minus everything else. Track every line item, accrue annual costs monthly, and stress-test for vacancy. Do that, and your numbers will tell you exactly when to raise rent, refinance, renovate, or sell.

Technology Tools for Effortless Income Tracking

Modern technology has revolutionized how investors track and manage their property income. From simple spreadsheets to sophisticated property management platforms, there are tools available for every level of investor.

Free Google Sheets Templates and Setup

Google Sheets offers a powerful, free solution for income tracking. Here's how to set up an effective system:

Essential Template Components:

- Monthly income tracker with automated calculations

- Expense categorization with dropdown menus

- Year-to-date summaries and trend analysis

- Budget vs. actual comparison charts

Setup Process:

- Create separate sheets for income, expenses, and dashboard summary

- Use data validation to create dropdown menus for expense categories

- Implement SUMIF formulas for automatic category totals

- Set up conditional formatting to highlight budget variances

Key Formulas for Automation:

- Total Monthly Income: =SUM(Income_Range)

- Category-Specific Expenses: =SUMIF(Category_Column, "Maintenance", Amount_Column)

- Net Income: =SUM(Income_Range) - SUM(Expense_Range)

- Year-to-Date Performance: =SUMIFS(Amount_Column, Date_Column, ">="&DATE(YEAR(TODAY()),1,1))

Professional Property Management Software

For investors seeking more automation and advanced features, professional software platforms offer comprehensive solutions.

Keyper - Dubai-Specific Platform: Keyper is specifically designed for Dubai landlords and offers integration with local systems like DLD and Ejari. Key features include:

- Automated rent tracking with Ejari integration

- Service request management

- Legal compliance monitoring

- Credit card rent payment processing

- Comprehensive financial reporting

- Mobile app for on-the-go management

Stessa - International Platform: Stessa provides free property management software with robust income tracking capabilities:

- Direct bank account integration

- Automated transaction categorization

- Tax reporting and preparation tools

- Portfolio performance analytics

- Expense receipt scanning and storage

Rental Yield and ROI Calculators

Before investing, use online calculators to estimate potential returns:

Available Platforms:

- Positive Properties UAE Rental Yield Calculator

- DAMAC Properties ROI Calculator

- SmartCrowd Investment Calculator

- McCone Properties Rental Calculator

These tools allow you to input purchase price, estimated rental income, and operating costs to get instant yield calculations.

Strategies to Maximize Rental Income

Maximizing rental income from your Dubai property investment involves a combination of strategic planning, proactive management, and understanding market dynamics. Beyond simply setting a competitive rent, several approaches can enhance your property's appeal and profitability.

1. Strategic Property Selection:

The foundation of high rental income begins with the initial investment. Properties in prime locations, particularly those near business hubs, metro stations, and tourist attractions, tend to deliver higher rental yields. Areas like Downtown Dubai, Dubai Marina, and Jumeirah Village Circle consistently show strong rental demand. Additionally, smaller units such as studios and one-bedroom apartments often achieve higher returns per square foot due to consistent rental demand.

2. Enhance Property Appeal:

A well-maintained and aesthetically pleasing property can command higher rents and attract quality tenants. Consider:

- Furnishing and Amenities: Fully furnished units with modern facilities can command premium rents. Investing in quality appliances, contemporary furniture, and smart home features can significantly increase your property's attractiveness.

- Regular Maintenance: Proactive maintenance prevents minor issues from escalating into costly repairs, ensuring tenant satisfaction and minimizing vacancy periods.

- Upgrades and Renovations: Strategic upgrades, such as kitchen or bathroom renovations, can increase property value and justify higher rental rates. Focus on improvements that offer a good return on investment.

3. Optimize Rental Pricing:

While market research helps set initial rent, continuous optimization is key. Monitor local rental trends and adjust your pricing accordingly. If the market is experiencing an upward trend, as seen in Dubai with average yearly rents increasing by 20.8% (Source: Emirates NBD), you may be able to increase your rent upon lease renewal. Utilize online rental calculators and consult with local real estate agents to ensure your pricing remains competitive yet maximizes your income.

4. Minimize Vacancy Periods:

Every day your property is vacant, you lose potential income. Strategies to minimize vacancies include:

- Proactive Marketing: Begin marketing your property well in advance of a tenant's departure.

- Efficient Tenant Screening: Thoroughly vet potential tenants to ensure reliability and reduce the likelihood of early lease termination.

- Excellent Tenant Relations: Happy tenants are more likely to renew their leases, reducing turnover costs and vacancy periods.

5. Consider Short-Term Rentals:

In certain high-demand areas, offering your property for short-term rentals (e.g., through platforms like Airbnb) can generate significantly higher income than long-term leases, especially during peak tourist seasons. However, this strategy comes with increased management responsibilities and potentially higher operational costs.

6. Leverage Property Management Services:

While property management fees are an expense, a professional management company can often maximize your net income by efficiently handling tenant acquisition, rent collection, maintenance, and legal compliance. Their expertise can lead to higher occupancy rates and optimized rental pricing, ultimately boosting your overall returns.

By implementing these strategies, property investors in Dubai can not only calculate and track their monthly income but also actively work towards enhancing their property's profitability and ensuring a robust return on investment.

Market Trends and Income Projections for 2025-2026

Understanding market trends is crucial for accurate income projections and investment planning.

Current Market Dynamics

Dubai's rental market continues to show strong fundamentals in 2025:

- Average rental yields remain stable at 6.7% across most areas (Source: Deloitte)

- Premium locations like Dubai Marina and Downtown Dubai command higher yields

- Emerging areas like Dubai South and Mohammed Bin Rashid City offer growth potential

- Government initiatives continue to support market stability

Income Growth Projections

Based on current market analysis and expert forecasts:

- Rental rates are expected to grow 3-5% annually in established areas. It already grew by 4.7% in Q3 of 2025 (Source: National news).

- New developments may see higher initial yields as they establish market presence

- Infrastructure improvements (Metro extensions, new attractions) will positively impact nearby property values

- Population growth and tourism recovery support continued rental demand

Risk Factors to Monitor

Successful income tracking must account for potential risks:

- Market oversupply in certain segments

- Economic fluctuations affecting tenant demand

- Regulatory changes impacting rental laws

- Global economic conditions affecting expatriate population

FAQ Section

Q1: What is the primary difference between Gross and Net ROI for Dubai properties?

A1: Gross ROI is a quick measure based solely on annual rental income versus purchase price, not accounting for any expenses. Net ROI, however, provides a more realistic view by subtracting all recurring property costs, such as service charges, maintenance, and management fees, from the rental income before calculating the return. Net ROI is crucial for accurate financial planning.

Q2: What are the most significant expenses to consider when calculating net income from a Dubai property?

A2: Key expenses include service charges for building maintenance, property management fees if you use a service, agency fees for tenant acquisition, and mortgage interest if the property is financed. It's also wise to factor in potential vacancy periods and a budget for unexpected repairs to ensure a realistic financial projection.

Q3: How can I track my monthly income and expenses efficiently for my Dubai property?

A3: You can use detailed spreadsheets to manually track income and expenses, categorizing each transaction. For more comprehensive management, consider property management software that automates rent collection, expense logging, and generates financial reports. Integrating with accounting software like QuickBooks can also provide a holistic financial overview for tax purposes.

Q4: Which areas in Dubai offer the highest rental yields for property investors?

A4: Areas like International City, Dubai Sports City, Dubai Silicon Oasis, and Jumeirah Village Circle (JVC) have historically shown high gross rental yields, often exceeding 8%. Emerging suburban communities such as Dubai South and Dubai Hills Estate are also gaining popularity due to strong growth in sales and rentals, offering attractive opportunities for investors.

Q5: What strategies can help maximize the rental income from my Dubai property?

A5: To maximize income, strategically select properties in high-demand locations, enhance property appeal through furnishing and regular maintenance, and optimize rental pricing based on market trends. Minimizing vacancy periods through proactive marketing and efficient tenant screening, and considering professional property management services, can also significantly boost your net returns.

Q6: How often should I recalculate my property's ROI in Dubai?

A6: It is advisable to recalculate your property's ROI at least annually, or more frequently if there are significant changes in market conditions, rental income, or expenses. Regular recalculation helps you stay informed about your investment's performance, identify trends, and make timely adjustments to your strategy to maintain profitability.

Deed's Take: Simplifying Income Tracking Through Fractional Investment

For many investors, the complexities of calculating and tracking monthly income from wholly-owned properties can be overwhelming. This is where fractional investment platforms like Deed are transforming the investment landscape.

Deed's approach eliminates the traditional hassles of property ownership while providing transparent, predictable monthly income. Our platform handles all aspects of property management, from tenant screening and rent collection to maintenance and legal compliance. Investors receive detailed monthly statements showing their proportional share of rental income, minus operating expenses and management fees.

The technology behind our platform automates income calculations and provides real-time portfolio performance tracking. With investments starting from just AED 500, Deed makes professional-grade real estate investment accessible to a broader range of investors. Our DFSA-regulated platform ensures transparency and compliance, giving investors confidence in their monthly income streams.

By choosing fractional investment through Deed, investors can focus on building their portfolios rather than managing individual properties. This approach is particularly valuable for busy professionals, international investors, or those seeking diversified exposure to Dubai's real estate market without the operational complexities.

Conclusion

Calculating and tracking monthly income from your Dubai property investment is not just a best practice; it is an indispensable element of successful real estate ventures. By diligently applying the principles of gross and net ROI, meticulously accounting for all expenses, and leveraging effective tracking tools, investors can gain unparalleled clarity into their property's financial performance. This proactive approach enables informed decision-making, allowing you to adapt to market dynamics, optimize your returns, and safeguard your investment.

Dubai's real estate market continues to offer compelling opportunities for those equipped with the right knowledge and strategies. Whether you are a seasoned investor or just beginning your journey, understanding the true profitability of your assets is paramount. Take control of your investment future today. Begin by implementing these calculation and tracking methods, and consider consulting with a reputable Dubai real estate expert to tailor a strategy that aligns with your financial goals. Your path to consistent and maximized monthly income from Dubai property investments starts now.

__________________________________________________

For promotional purposes only. Property and other details may vary. Capital at risk. Deed is regulated by the DFSA.

Senior Growth, Marketing & Brand Manager | Elevating Brand Equity & Fueling Sales Growth Across Fintech, Proptech.

Signup to our newsletter!

Stay ahead with exclusive updates, insights, and opportunities delivered straight to your inbox.

Frequently Asked Questions

Start earning passive income today

Join thousands of investors building wealth through fully-managed rental properties.